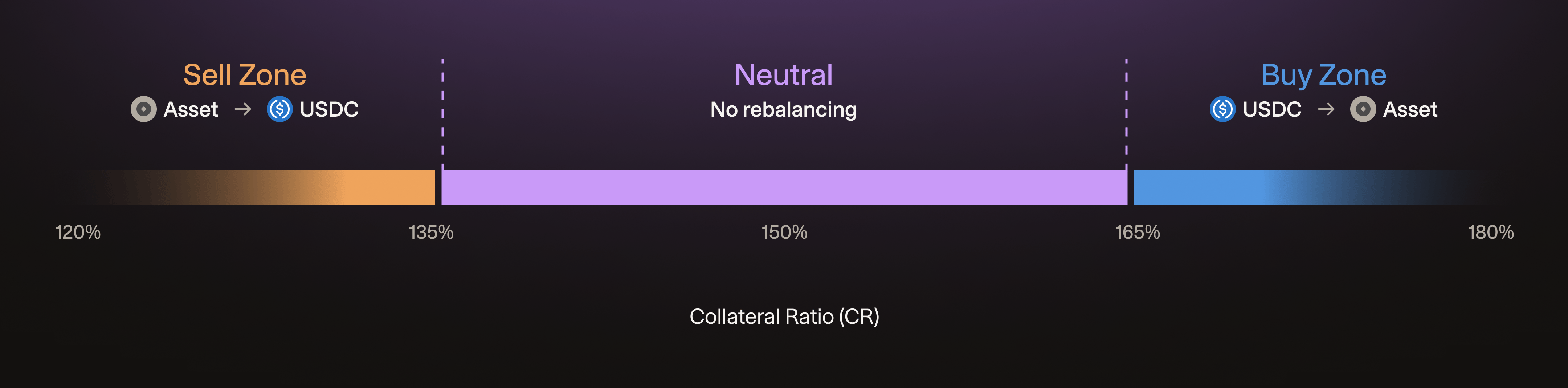

Rebalancing Zones

Each volatile collateral pool (e.g. SOL, BTC) has two rebalancing zones:- Sell Zone: at low CR, the protocol sells collateral for USDC to derisk

- Buy Zone: at high CR, the protocol buys more collateral with USDC

Rebalancing routes are per-pair and independent: one pair can be selling collateral while another is buying.

Sell Zone

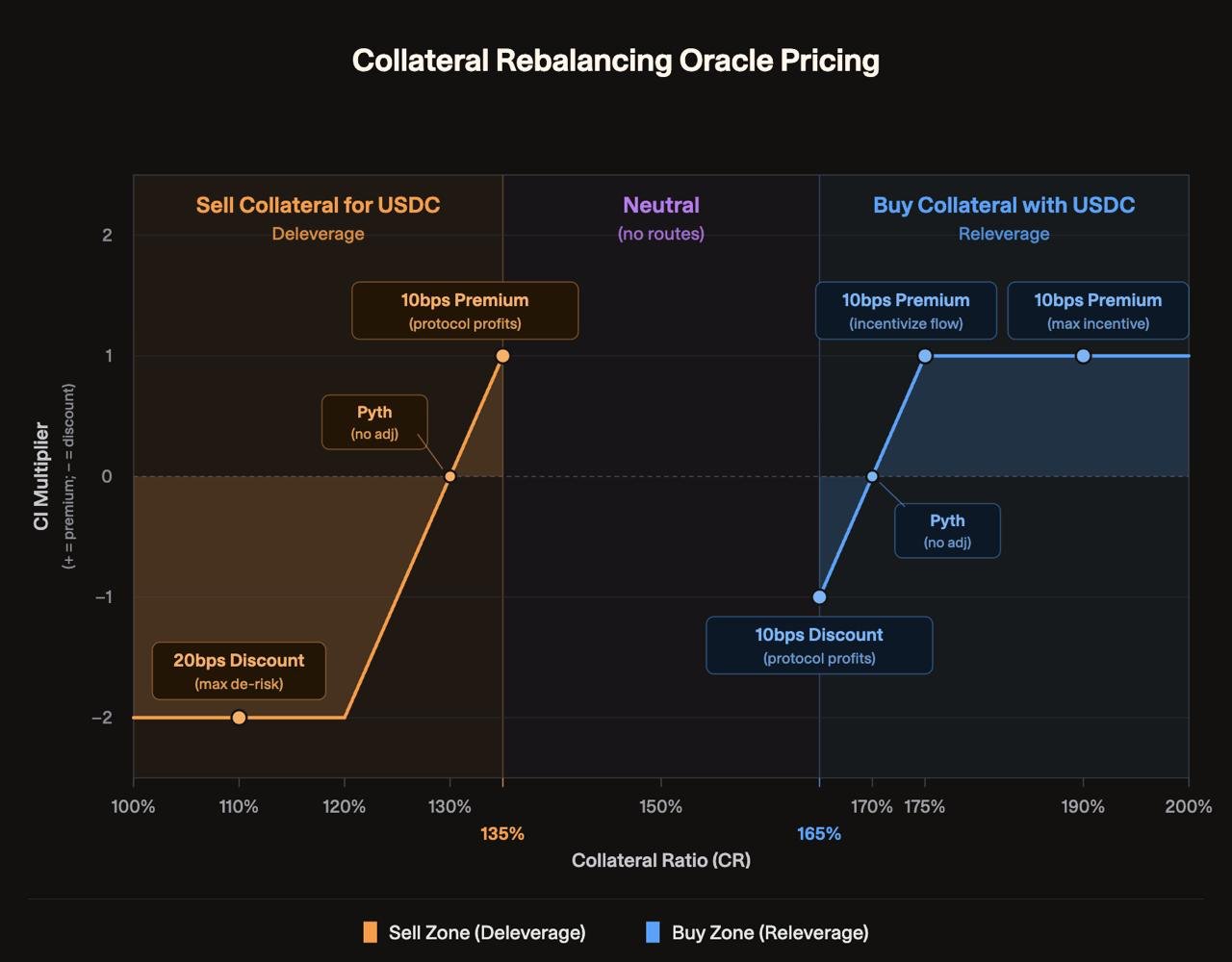

When a pool’s CR drops into the sell zone, the protocol opens an ASSET → USDC route. This sells collateral from the stressed pool and moves its backing into USDC, de-leveraging the xASSET and raising the pool’s CR toward 135%. The amount of collateral available for sale is capped to avoid overshooting past the sell zone inner bound. The zones are asymmetric: the sell-side pricing bands span a wider CR range (135% down to 100%) than the buy-side band (165% to 175%), because de-risking under stress demands a more graduated response.Buy Zone

When a pool’s CR rises into the buy zone, the protocol opens a USDC → ASSET route for arbitrageurs. This deploys USDC reserves to purchase more collateral, simultaneously re-leveraging the xASSET and bringing the pool’s CR down toward 165%. The amount of buyable collateral is similarly capped to prevent overshooting. See Hylo Equations for the max sellable and buyable formulas.Rebalance Pricing

Rebalance pricing applies a percentage spread to the oracle spot price that scales with how much the pool needs the flow:- Near the inner bound (CR close to target), the protocol rebalances at a profit, selling collateral above spot or buying below it, since the pool barely needs the flow

- At a crossover point partway through the zone, the protocol rebalances at break-even, exactly at oracle spot: no profit, no subsidy

- At the outer bound (pool most stressed), the protocol rebalances at a subsidy (a discount on collateral in the sell zone, a premium in the buy zone), paying counterparties to provide the flow it now urgently needs

- Beyond the outer bound, the spread clamps flat; beyond the inner bound, the route deactivates

Profit and Loss Settlement

Every rebalance settles its profit or subsidy against the Earn Pool by minting or burning hyUSD:- A rebalance executed at a profit mints hyUSD into the Earn Pool

- A rebalance executed at a subsidy burns hyUSD from the Earn Pool

Virtual Stablecoin Accounting

Rebalancing routes adjust the virtual stablecoin supply across pools:- Sell (ASSET → USDC): burns vUSD on the volatile pair, mints vUSD on the USDC pair

- Buy (USDC → ASSET): burns vUSD on the USDC pair, mints vUSD on the volatile pair